Images Money via Flickr

Public Debt: From a Stopgap to a Threat?

Jörn Quitzau

Bergos AG

Joern Quitzau is a Geoeconomics Non-Resident Senior Fellow at AGI. He is Chief Economist at Bergos, a private bank based in Switzerland. He specializes in economic trend research and economic policy. Joern Quitzau hosts two Economics podcasts.

Prior to his position at Bergos, Joern Quitzau worked for Berenberg in Hamburg (2007-2024) and Deutsche Bank Research in Frankfurt (2000-2006) with a special focus on tax and fiscal policy.

Dr. Quitzau (PhD, University of Hamburg) was a Visiting Fellow at AGI in April 2014 and September 2022 and an American-German Situation Room Fellow in April 2018.

Mickey Levy

Dr. Mickey Levy for many years was Chief Economist at Bank of America, followed by Berenberg Capital Markets. He is a long-standing member of the Shadow Open Market Committee and is a Visiting Scholar at the Hoover Institution at Stanford University.

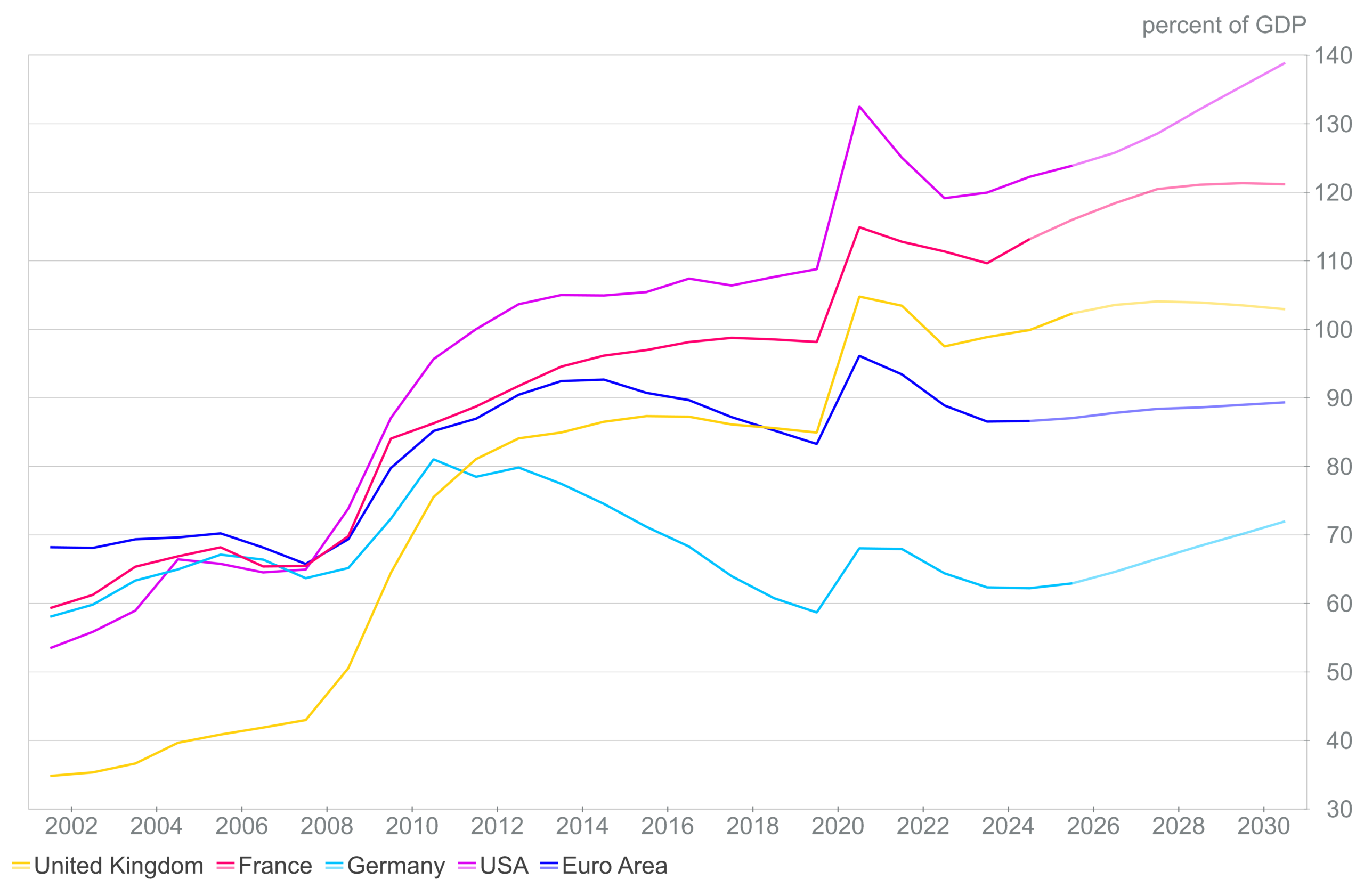

Public debt is in the spotlight. According to the IMF, global public debt stands at 93 percent of global gross domestic product (GDP). By the end of the decade, IMF projections indicate that debt will rise to over 100 percent of global GDP. That would be the highest level since 1948. Many major economies are heavily indebted, including Japan (debt-to-GDP ratio: 230 percent), the United States (125 percent), Canada (114 percent), the United Kingdom (103 percent), France (116 percent), and Italy (137 percent). Is this becoming dangerous? That depends on lenders’ confidence in the respective country’s ability and willingness to repay.

Reasons for Government Debt

First of all: government debt is not inherently bad. Deficit spending is appropriate to cushion short-term slumps in demand and stabilize the economy. However, governments should aim to balance deficits and surpluses over the course of business cycles. Deficit spending that finances activities and investments that raise longer-run growth and increase the number of future taxpayers are also part of healthy public finance. Obviously, the ongoing budget deficits and cumulative government debt violate these recommended tenets of sound public finance.

Debt Is Politically More Appealing Than Taxes

The story behind the massive debt buildup is a different one. Rising debt and borrowing are easy ways for politicians to conceal financial burdens. While taxes and fees to finance public goods and services are immediately felt, they can be deferred into the future through loan financing. This fiscal illusion of deferring the costs of current spending is what makes debt financing so appealing to politicians.

Since politicians tend to think in terms of election cycles, short-term actions dominate. Available funds that satisfy the demands of key voter groups are not always used for what is best for economic performance in the long term. Despite high revenues, Germany has long neglected its traditional government responsibilities—national security, defense, infrastructure, and education. The shortcomings in these areas must now be corrected in a short period of time. And, as is so often the case, increased borrowing serves as a stopgap. A year ago, the German debt brake was specifically relaxed to give the federal government more financial leeway.

Implicit Debt

In the major industrialized nations, demographic trends are exacerbating the debt problem. As the “baby boomers” enter retirement, valuable workers are leaving the labor market, and the financial burdens lurking within social security systems are readily apparent. Government budgets are measured and reported on a cash flow basis. The term “implicit” or “hidden” debt is used when the social benefits promised by the government for the future (for old age, health, and long-term care) are not covered by corresponding future revenues. Implicit debt is not recognized in government cash flow budgets; it has not yet been securitized and therefore plays no role in the capital markets.

However, if conditions remain unchanged—without structural reforms, benefit cuts, or increases in taxes and fees—the German government will have to take on new debt in the future to meet its benefit commitments to citizens. Calculations by the Stiftung Marktwirtschaft suggest that implicit debt in Germany amounts to nearly 400 percent of gross domestic product (GDP). This is many times the official national debt, which is based on cash flows and currently stands at just under 65 percent of GDP.

The fact that implicit debt gradually turns into explicit debt is not an inevitable fate. Higher contributions and, above all, a higher retirement age could alleviate the problem. Yet the demographic challenges have been known for decades, without any corresponding shift in international economic policy. Efficient and fair public finances require changes in anticipation of demographic realities.

A World in Transition: No Time for Sustainable Fiscal Policy?

The rise in public debt can no longer be explained solely by politicians’ usual fiscal laxity. Speed clearly plays a key role in the economic and political realignment of the world. Balanced public budgets are not the top priority when, as in Europe, the focus is on rapidly restoring defense capabilities. Lax fiscal policy is widespread: advanced economies are expected to record average budget deficits of around 5 percent of GDP this year.

Government debt service costs are being pushed up by higher interest rates. High government debt can become a risk. This exacerbates the risks in the current situation by raising the risks associated with government bonds. Such risks to international financial stability stemming from high government debt are mounting. Recently, there has been discussion in Europe about the vulnerability of the United States should major bond investors sell off large amounts of U.S. Treasury bonds.

U.S. Debt

Indeed, the United States is highly indebted, with total government debt just over 120 percent of GDP. Net interest costs now exceed $1 trillion per year, or 14 percent of total federal spending. Whether it is sustainable depends on economic growth, an eventual political compromise that leads to a flattening of government spending, and the willingness of domestic and foreign creditors to continue holding U.S. government bonds.

One of the potential risks is that the U.S. government debt rises to a point that it begins to dominate financial markets and forces the Federal Reserve to lower interest rates, which would lead to higher inflation. While the U.S. Treasury markets continue to function in a healthy manner, the potential for fiscal burdens to mount and begin influencing financial markets deserves attention.

U.S. sustainable potential growth remains healthy, by most estimates the strongest among all advanced economies. This lifts higher standards of living and fuels government revenues. Of note, unlike many EU nations, the U.S. tax system is indexed for inflation such that higher inflation does not improve the budget.

Total U.S. government outstanding debt is $38.5 trillion. $7.5 trillion is held in U.S. government accounts such as the Social Security trust funds. In addition, the Federal Reserve’s balance sheet holds $4.4 trillion in US treasuries. Of the remaining $26.6 trillion of publicly-held debt, foreign institutions—both private and sovereign—hold $9.25 trillion, or 34.8 percent, while $17.35 trillion is held by various U.S. creditors. This is far different than Japan, where over 90 percent of the debt is held by domestic creditors.

The largest foreign holders of U.S. government debt include Japan, China, and OPEC nations whose primary source of revenue is oil, which is transacted in US dollars. A sizable portion of the U.S. treasury holdings of Middle East nations are domiciled in various other locations, including the Cayman Islands, Luxembourg, and the UK, so their origins are difficult to trace.

While there are concerns about whether U.S. government debt will maintain its high standing among global creditors, including sovereign and private holders of the debt securities, holding the U.S. debt has clear advantages over alternative assets. The U.S. dollar remains the world’s reserve currency, the U.S. government debt market is the world’s largest and most liquid, and U.S. Treasury yields are among the highest in the world. This reflects the U.S. economy’s high potential growth that is associated with higher rates of return. International capital flows to the highest risk-adjusted rates of return, which attracts foreign capital and maintains the attractiveness of holding U.S. treasury securities.

Risks are certainly apparent, and the situation may change. Concerns about U.S. debt, higher inflation, or worries that President Trump’s jarring diplomatic moves that call into question the reliability of the United States may reduce global acceptance of holding U.S. Treasury debt securities. Weakness in the U.S. dollar may reflect some of these worries. However, large holders of U.S. Treasuries fully understand that they would incur sizable capital losses if massive selling drove down the prices of Treasuries, and they must carefully weigh the potential costs of jarring portfolio adjustments.

Accordingly, by far the highest probability is continued growth in the U.S. Treasury market and its continued role of providing a safe haven in global financial markets.

This is an English version of “Die Welt versinkt im Schuldensumpf” which was first published in the Frankfurter Allgemeine Zeitung.