Turning Plans Into Action

Alexander Privitera

AGI Non-Resident Senior Fellow

Alexander Privitera a Geoeconomics Non-Resident Senior Fellow at AGI. He is a columnist at BRINK news and professor at Marconi University. He was previously Senior Policy Advisor at the European Banking Federation and was the head of European affairs at Commerzbank AG. He focuses primarily on Germany’s European policies and their impact on relations between the United States and Europe. Previously, Mr. Privitera was the Washington-based correspondent for the leading German news channel, N24. As a journalist, over the past two decades he has been posted to Berlin, Bonn, Brussels, and Rome. Mr. Privitera was born in Rome, Italy, and holds a degree in Political Science (International Relations and Economics) from La Sapienza University in Rome.

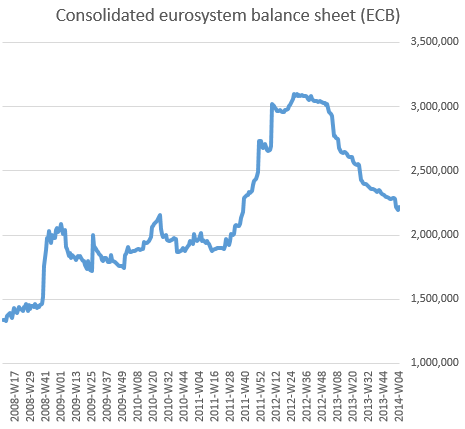

About a year ago, markets were experiencing serious taper tantrums. At the time, ECB President Mario Draghi proudly defended the fact that unwinding outright asset purchases, and therefore reducing its huge balance sheet, was only a challenge for the U.S. Federal Reserve (Fed), and not for the euro zone. Indeed, at the time, European banks were repaying loans they had received from the ECB in the form of generous long-term refinancing operations (LTROs) and the balance sheet of the central bank was shrinking very smoothly.

Fast-forward to September 2014, it is now quite clear that monetary conditions in the euro area have been too tight for over a year. This has contributed to support the euro exchange rate—one of the causes for the low inflation readings in past months. Hence, Draghi, backed by a comfortable majority of the governing council, has decided to expand the balance sheet of the ECB back to the levels of 2012. This would mean no less than pumping about a trillion euros into the economy—quite a reversal.

While it is unclear whether injecting additional liquidity would actually automatically boost lending activities to the real economy—and in fact the ECB’s LTROs failed to do so in the past—it should at the very least weaken the exchange rate of the euro. Indeed, while the ECB embarks on its own light version of quantitative easing (QE), the Fed is about to end its program of asset purchases completely and monetary conditions in the United States could tighten faster than anticipated, which is supportive for the dollar.

Things get trickier when trying to assess the effects of the latest ECB announcements on credit intermediation. Lending to small and medium-sized companies is still contracting in the euro zone. So far all attempts to boost credit flows have failed. The targeted longer refinancing operations (TLTROs) that the ECB is starting to offer this month could be supportive for lending activities, but only if banks take up the offer of cheap central bank money. Many analysts doubt that will the case, since the extra liquidity comes with strings attached—the banks have to lend the extra money to the real economy and they are still reluctant to do so. Even the ECB seems to share those doubts. This is why it is trying to stimulate demand for its TLTROs by lowering key interest rates further and, more importantly, by promising to buy repackaged loans from banks. However, buying bundled loans—or asset-backed securities (ABS)—from banks is not as straightforward as it may seem.

In fact, the ECB is about to become even more experimental than the Fed. In all QE rounds in the United States, the Fed targeted government-backed assets, either because it bought U.S. treasuries or mortgage-backed securities that were guaranteed by the government, or indeed both. The ECB would like to emulate the Fed’s approach, at least to some degree. It has asked euro zone member countries to guarantee parts of the central bank’s asset-purchase program unveiled last week. In other words, the ECB is trying to disperse some of the credit risk it is about to take on its balance sheet. It is one thing to relax collateral rules for banks that need ECB liquidity, quite another to outright purchase assets that may well turn sour.

According to Bloomberg News, the initial response to Draghi’s request to provide for some form of government guarantees for the ECB’s planned ABS purchases has been no. In a position paper to be presented to euro area finance ministers later this week, the French and German governments reportedly define such guarantees as “problematic.” The ECB can either decide to go ahead anyway and take on private sector risks that it had largely avoided so far, or it can insist on some mechanism of guarantees, most likely involving the European Investment Bank (EIB), Europe’s own development bank. But, this would make the EIB’s own balance sheet more vulnerable to shocks and jeopardize its current AAA credit rating. Alternatively, the ECB could ask the European Commission to come up with a scheme that reduces the risks the central bank is about to undertake. In either case, it is fair to assume that the balance sheet of the ECB is about to get more vulnerable.

Ultimately, this is the consequence of the fact that the euro zone still has no centralized fiscal authority, able to issue bonds and credible guarantees. Instead of addressing this blatant shortcoming, governments are still sitting on the sidelines, or worse, hiding behind the ECB. We know what the ECB would like to achieve. I am afraid that without the banks’ help and more decisive member countries’ governments’ support, the central bank will only manage to go so far.