Unwarranted Schadenfreude (or Why the Survival of the Euro Matters to Americans)

Schadenfreude [shahd-n-froi-duh] noun:

satisfaction or pleasure felt at someone else’s misfortune

It’s very tempting for Americans to roll their eyes about the debt crisis in Greece, and to treat the entire European euro crisis as a remote parlor game, where the success or failure of Greece to stay in the euro is a betting sport, but one which ultimately will not ruin the bettor. Sadly, however, that belief is fundamentally mistaken in this age of interdependence, and Americans should understand what is at stake, and help the euro zone to survive intact in whatever ways we can.

In the mid-2000s, European and U.S. policymakers alike were seduced by the notion that the successful creation of the euro had effectively de-coupled the European economies from the U.S.’. Because Europeans had wanted to become more independent of the dollar and the Bush administration’s “reckless” economic policies, they wanted to believe that any economic crisis would stop at the water’s edge, and the European economies could be cordoned off. They were wrong. When the subprime mortgage crisis hit and U.S. banks collapsed, the transmission to EU banks was instantaneous. Moreover, not only EU banks with unwise loans like Northern Rock were roiled–all banks were tarred and feathered as investors sought information about how bad things really were. A flaw in the EU’s oversight of the banking sector showed that literally no one could say quickly and accurately how much exposure to risky loans the multinational banks in Europe had in their portfolios. Overnight, the economic crisis was transmitted to the EU, and most Europeans never had a chance to enjoy their bit of Schadenfreude at the abrupt demise of the “Cowboy Capitalism” model.

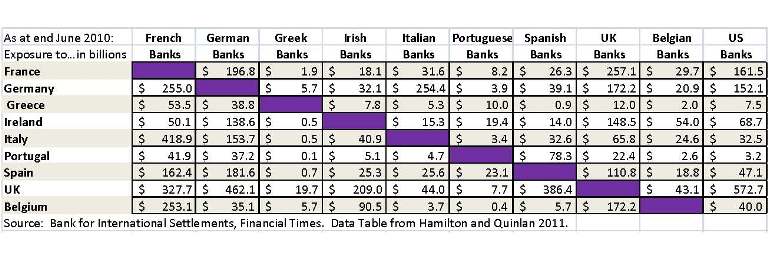

It’s a cautionary tale for Americans now. The U.S. seems finally to be digging out from its economic woes, and many people have the view that the euro is not part of their economic landscape and therefore they should not care one way or another about it. Yet the same instantaneous transmission mechanism–the interbank overnight lending market–is still active, and can carry chaos to the U.S. at any time. One change, however, is that this time we know where those problems are. Because better transparency and disclosure requirements have been implemented since 2007, we can identify which U.S. and European banks have what exposure to Greek sovereign euro debt. Fortunately, that number is relatively small ($7.5 billion). Unfortunately, in the age of interdependence, that’s not the end of the story as the graph below–taken from Hamilton and Quinlan’s The Transatlantic Economy 2011–makes clear. To understand the extent of U.S. banks’ exposure to Greek debt, one would have to include, for example, the large exposure that U.S. banks have to UK banks, and notice that UK banks have $12 billion exposure to Greek debt, and so forth. All told, most European banks have exposure to Greek debt, and if Greece were to default, many European banks would be at risk of being undercapitalized. This, in turn, would put pressure on U.S. banks with exposure to European banks, which hits all major banks. Thus, a Greek default would immediately–overnight–create a seizing up of the U.S. credit markets as all parties sorted out their credit risks and exposures.

Clearly, that’s not the end of the story either. Once Greece defaults on its euro obligations, the risk of a second or third sovereign default in Italy, Spain, or another state immediately becomes significantly higher, and financial markets react. In such a scenario, the economics literature tell us that markets are prone to overshooting, that is, going too far, judging the risks of another sovereign default too likely, and in the process, creating a self-fulfilling proposition. By bidding up the interest rates demanded on Italian eurobonds to unsustainable levels, the financial markets begin to make default inevitable and become part of the problem regardless of the underlying real economy.

A quick look at the table below suffices to show that U.S. exposure to Italian banks (and the other EU banks’ exposures to Italian euro debt and banks) is not a negligible amount. Thus even the whiff of contagion can be very bad for the credit markets and the overnight banking system.

All of these financial market risks ultimately play out in the real economy as well. As the U.S. has learned, living with an undercapitalized banking system is a significant barrier to robust economic growth in the real economy. Banks reduce lending in order to shore up their capital ratios, and even solid, creditworthy companies have a difficult time finding credit. Financial market turmoil creates uncertainty, and uncertainty does not lead to business investment needed to grow and to create jobs.

In a very real way, every American has a stake in whether or not the euro survives. On a very intuitive level, U.S. exporters lose when their markets are in recession. But more importantly, the economic chaos created by the ejection of any euro member would reverberate around the world, and certainly would affect the U.S. significantly beyond lost exports.

Some in the U.S. believe Greece ultimately should not be in the euro zone, because its economy is too different from the others’ and its growth is being strangled by participation in the euro. Even if that were true, however, it’s worth remembering the principle that big changes should never be made during a crisis period because of market effects like contagion and overshooting. In the long run, slow, negotiated, out-of-the-public-eye change is possible, so saving Greece right now does not necessarily imply that Greece’s economy has to be straight-jacketed in the euro forever. For now, however, all oars need to be in the water, rowing in the same direction, and that means the U.S. also needs to help the euro survive, whether it’s helping to motivate IMF assistance or encouraging the Federal Reserve to accept new collateral or giving the euro rhetorical support.

As tempting as Schadenfreude at the euro’s troubles is for Americans, now is not the time to indulge.

Click here for table depicting select European nation’s exposure to foreign banks

{kind=link}